Designing Stock Exchange

· 20 min read

Requirements

- order-matching system for

buyandsellorders. Types of orders:- Market Orders

- Limit Orders

- Stop-Loss Orders

- Fill-or-Kill Orders

- Duration of Orders

- high availability and low latency for millions of users

- async design - use messaging queue extensively (btw. side-effect: engineers work on one service pub to a queue and does not even know where exactly is the downstream service and hence cannot do evil.)

Architecture

Components and How do they interact with each other.

order matching system

- shard by stock code

- order's basic data model (other metadata are omitted):

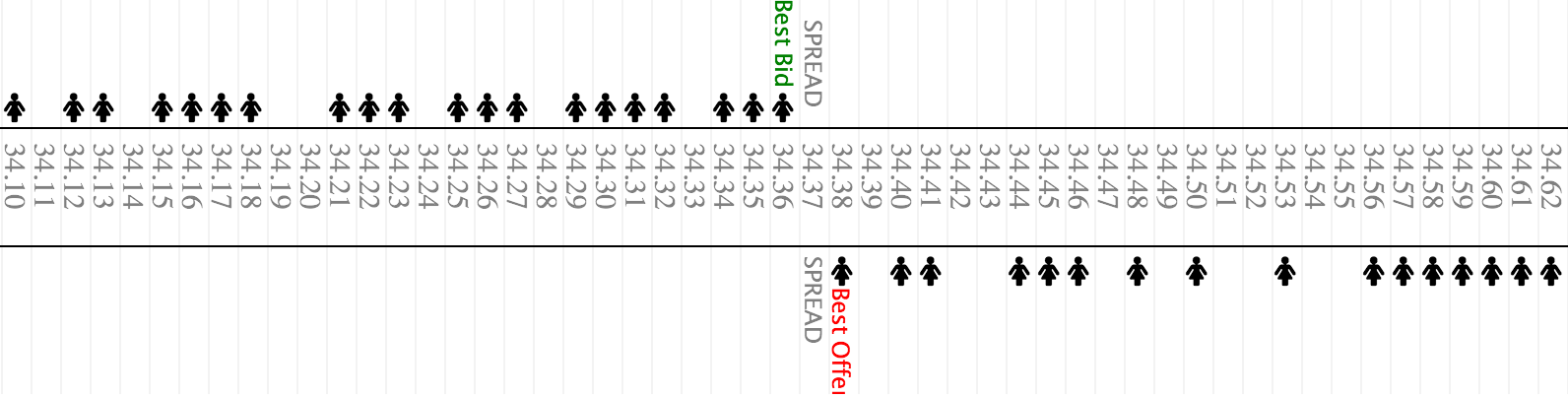

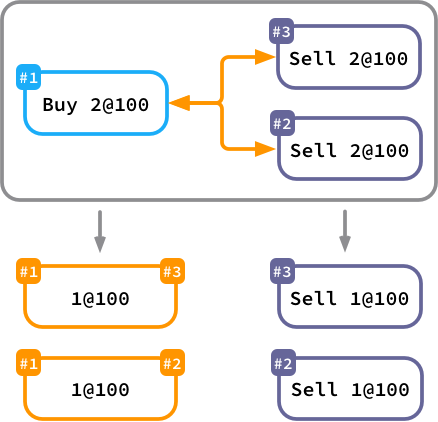

Order(id, stock, side, time, qty, price) - the core abstraction of the order book is the matching algorithm. there are a bunch of matching algorithms(ref to stackoverflow, ref to medium)

- example 1: price-time FIFO - a kind of 2D vector cast or flatten into 1D vector

- x-axis is price

- y-axis is orders. Price/time priority queue, FIFO.

- Buy-side: ascending in price, descending in time.

- Sell-side: ascending in price, ascending in time.

- in other words

- Buy-side: the higher the price and the earlier the order, the nearer we should put it to the center of the matching.

- Sell-side: the lower the price and the earlier the order, the nearer we should put it to the center of the matching.

x-axis

with y-axis cast into x-axis

Id Side Time Qty Price Qty Time Side

---+------+-------+-----+-------+-----+-------+------

#3 20.30 200 09:05 SELL

#1 20.30 100 09:01 SELL

#2 20.25 100 09:03 SELL

#5 BUY 09:08 200 20.20

#4 BUY 09:06 100 20.15

#6 BUY 09:09 200 20.15

Order book from Coinbase Pro

The Single Stock-Exchange Simulator

- example 2: pro-rata

How to implement the price-time FIFO matching algorithm?

- shard by stock, CP over AP: one stock one partition

- stateful in-memory tree-map

- periodically iterate the treemap to match orders

- data persistence with cassandra

- in/out requests of the order matching services are made through messaging queues

- failover

- the in-memory tree-maps are snapshotting into database

- in an error case, recover from the snapshot and de-duplicate with cache

How to transmit data of the order book to the client-side in realtime?

- websocket

How to support different kinds of orders?

- same

SELL or BUY: qty @ pricein the treemap with different creation setup and matching conditions- Market Orders: place the order at the last market price.

- Limit Orders: place the order with at a specific price.

- Stop-Loss Orders: place the order with at a specific price, and match it in certain conditions.

- Fill-or-Kill Orders: place the order with at a specific price, but match it only once.

- Duration of Orders: place the order with at a specific price, but match it only in the given time span.

Orders Service

- Preserves all active orders and order history.

- Writes to order matching when receives a new order.

- Receives matched orders and settle with external clearing house (async external gateway call + cronjob to sync DB)

References

- How Exchange Happen? Simulating a financial exchange in Scala

- Open Sources

- The Financial Information eXchange ("FIX") Protocol

- Types of orders: Technical Analysis Course. Training,Coaching & Mentoring for Traders / Investors - Types of orders used when buying or selling a stock

- GitHub - fmstephe/matching_engine: A simple financial trading matching engine. Built to learn more about how they work.

- Automated Algorithmic Trading: Learning Agents for Limit Order Book Trading